Introduction to Accumulated Depreciation

Accumulated depreciation is a fundamental concept in accounting, representing the total depreciation that has been recorded over time against a fixed asset. It reduces the asset’s book value on the balance sheet and is an essential indicator of the asset’s aging process. This concept helps companies understand how much of an asset’s cost has been allocated as an expense over its useful life.

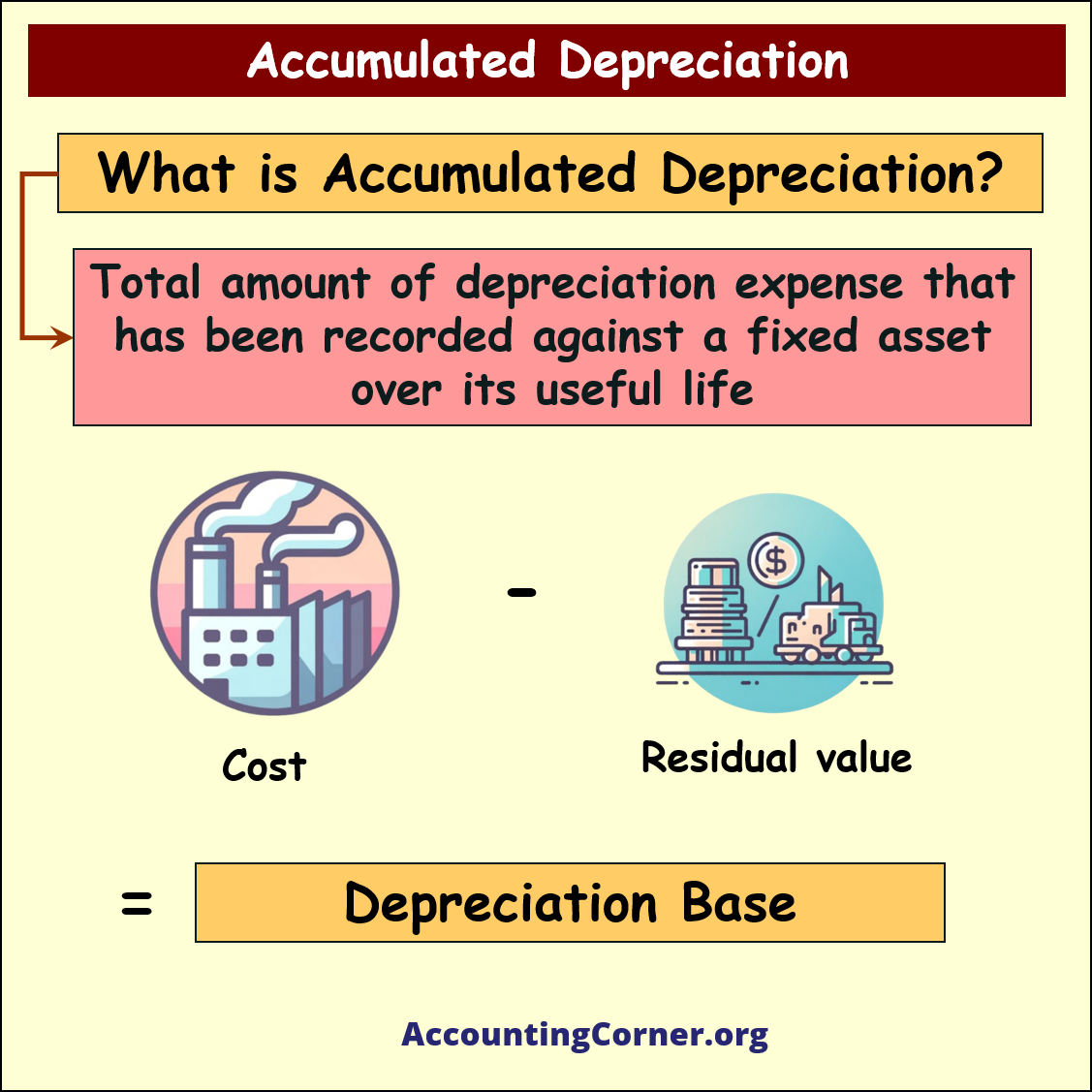

What is Accumulated Depreciation?

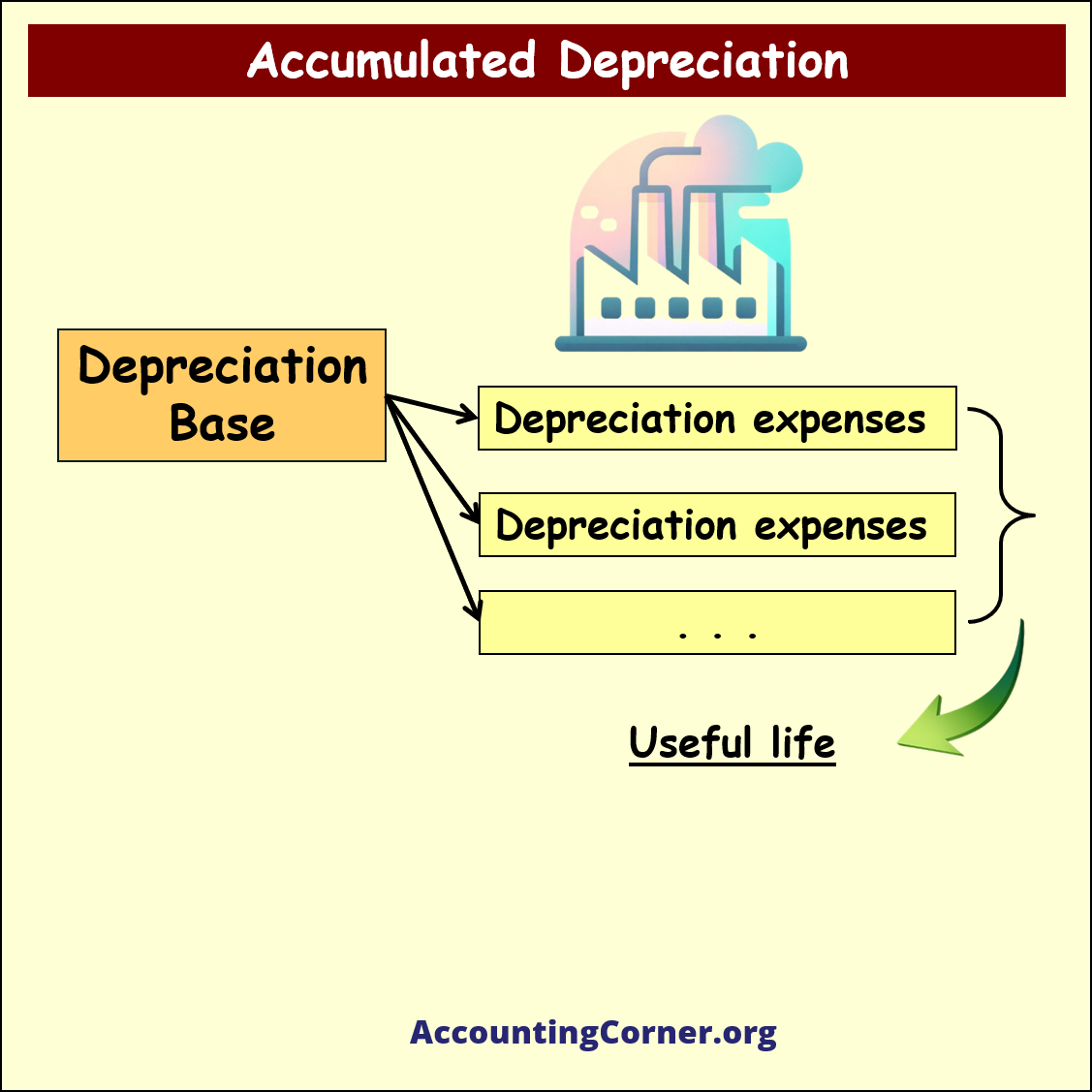

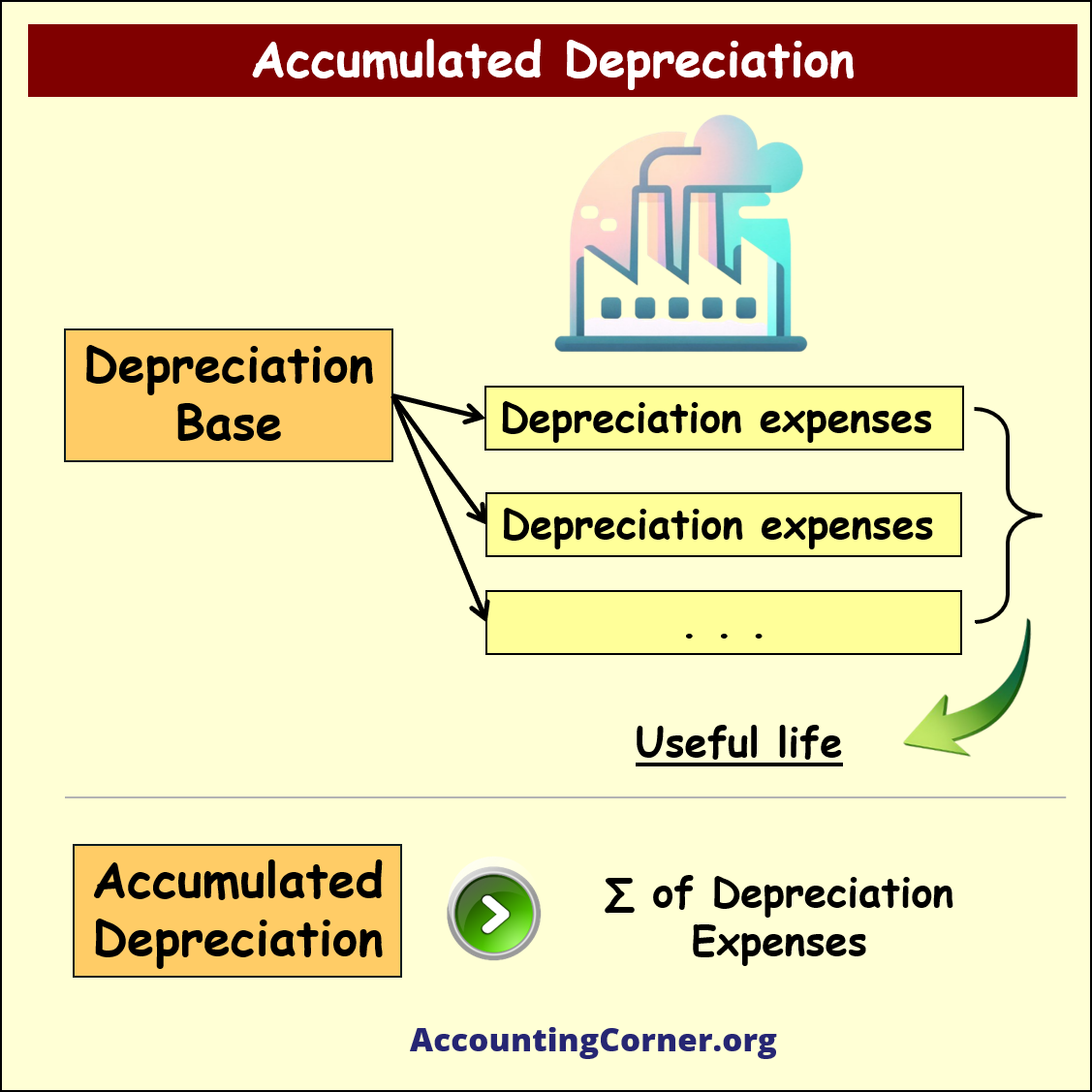

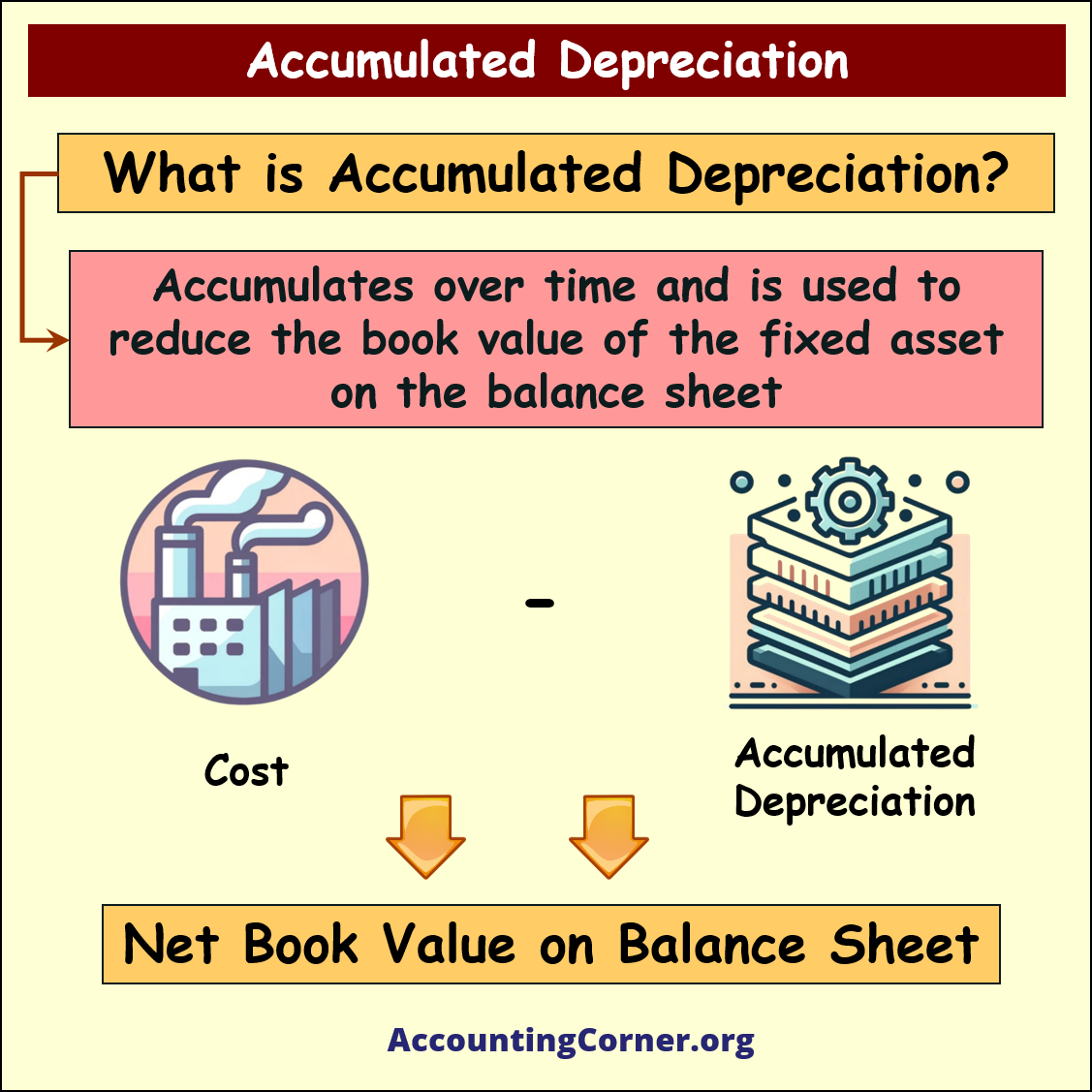

Accumulated depreciation refers to the total amount of depreciation expense charged against a fixed asset since it was put into service. It accumulates over the asset’s useful life and helps reduce the asset’s book value on the balance sheet.

Key Formula for Depreciation Base:

- Depreciation Base=Cost of Asset−Residual Value

The depreciation base is divided over the useful life of the asset, which determines the annual depreciation expense.

Key Features of Accumulated Depreciation:

- Total Depreciation Recorded: Represents the sum of all depreciation expenses charged against the asset since its acquisition.

- Reduces Book Value: The asset’s cost is reduced by the accumulated depreciation, showing the net book value on the balance sheet.

- Accumulates Over Time: Each year’s depreciation adds to the total accumulated depreciation.

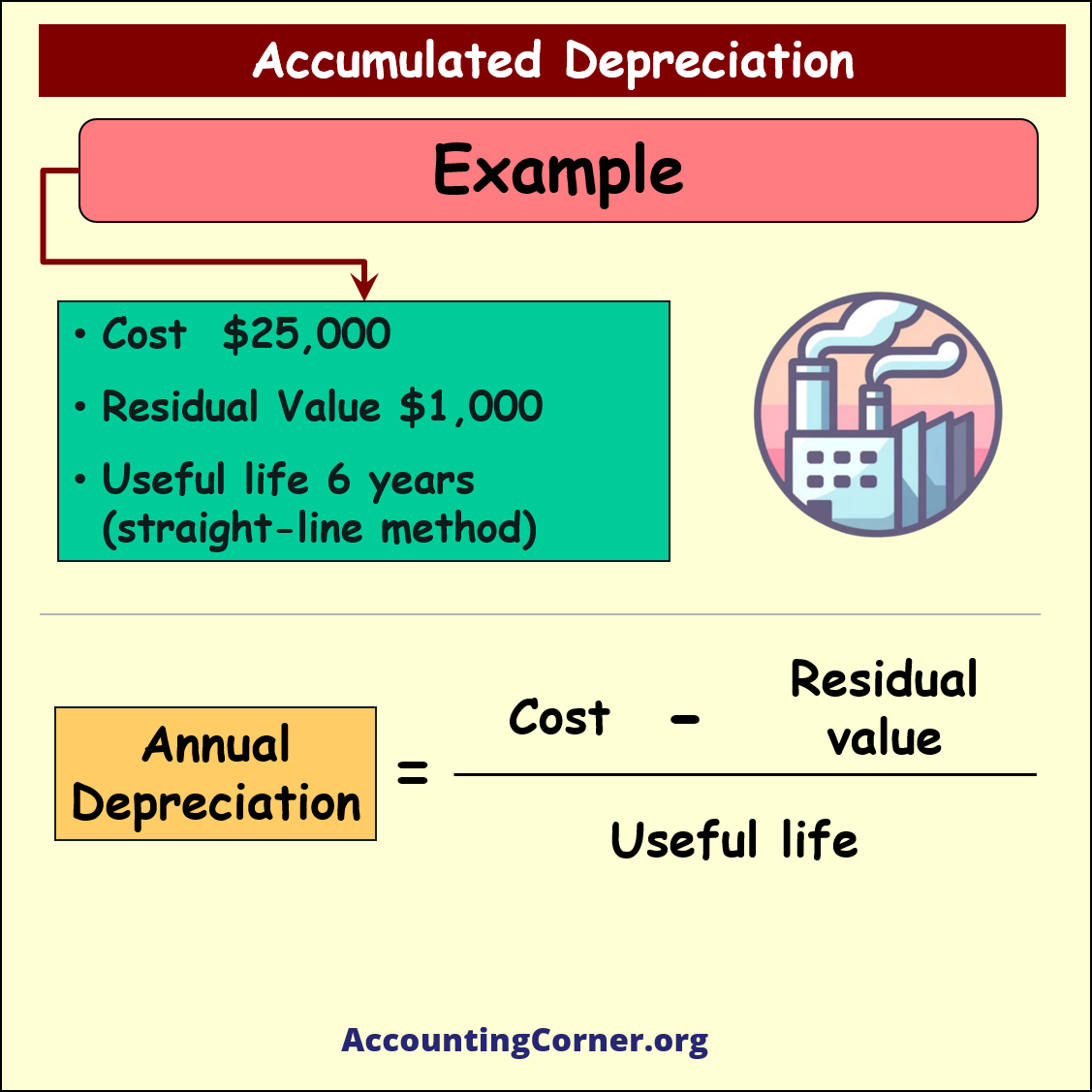

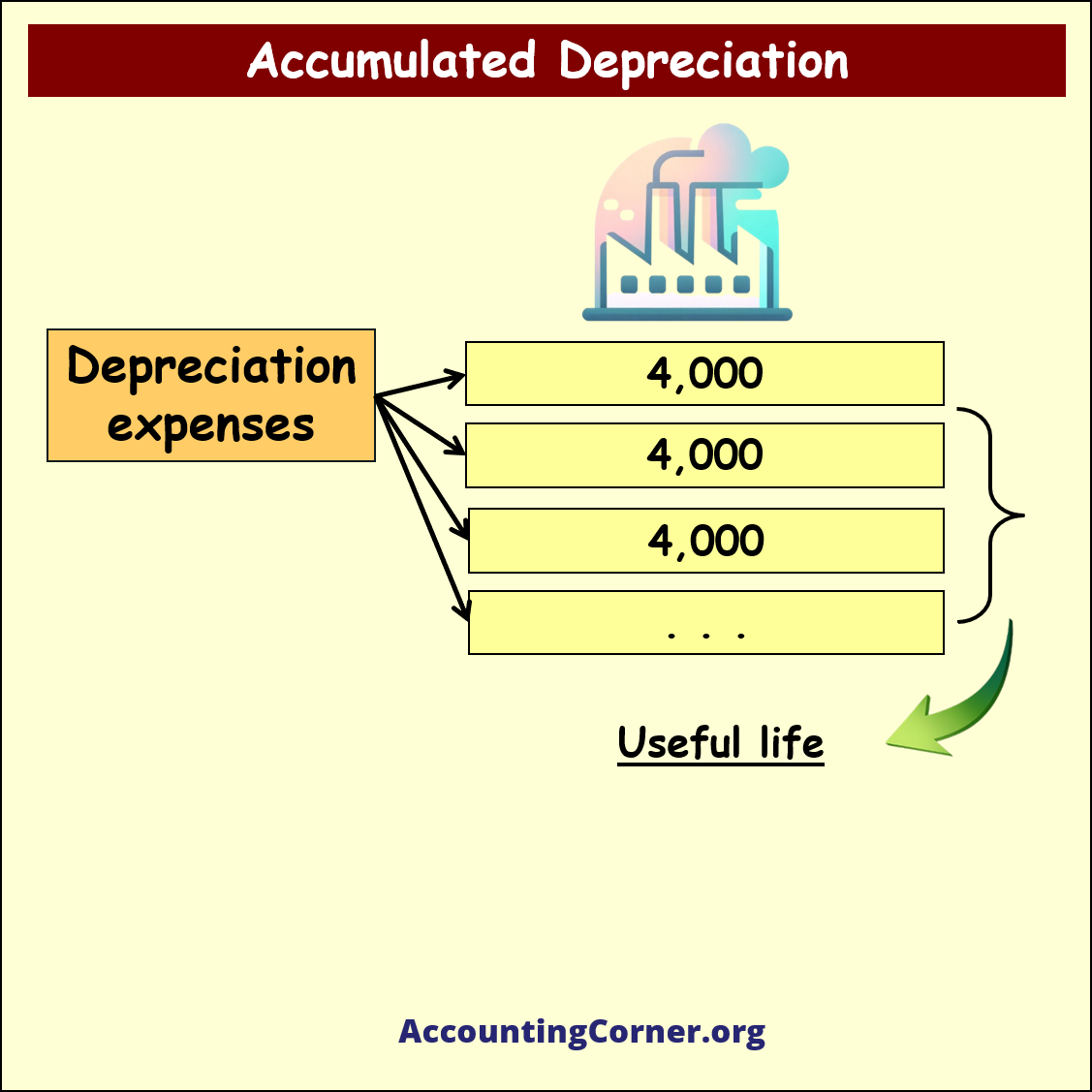

Example of Accumulated Depreciation

To illustrate accumulated depreciation, let’s consider an asset with the following details:

- Cost: $25,000

- Residual Value: $1,000

- Useful Life: 6 years (using the straight-line depreciation method)

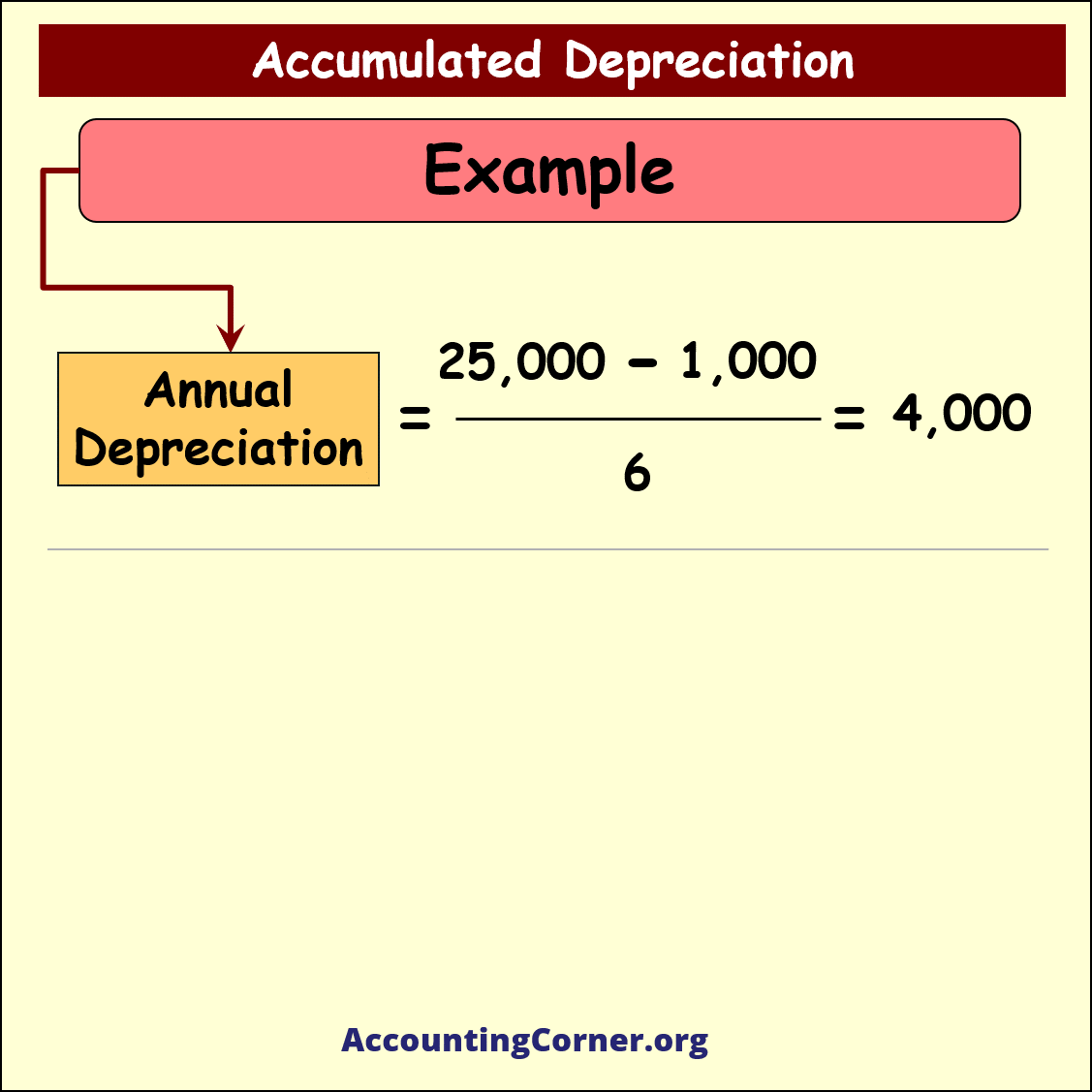

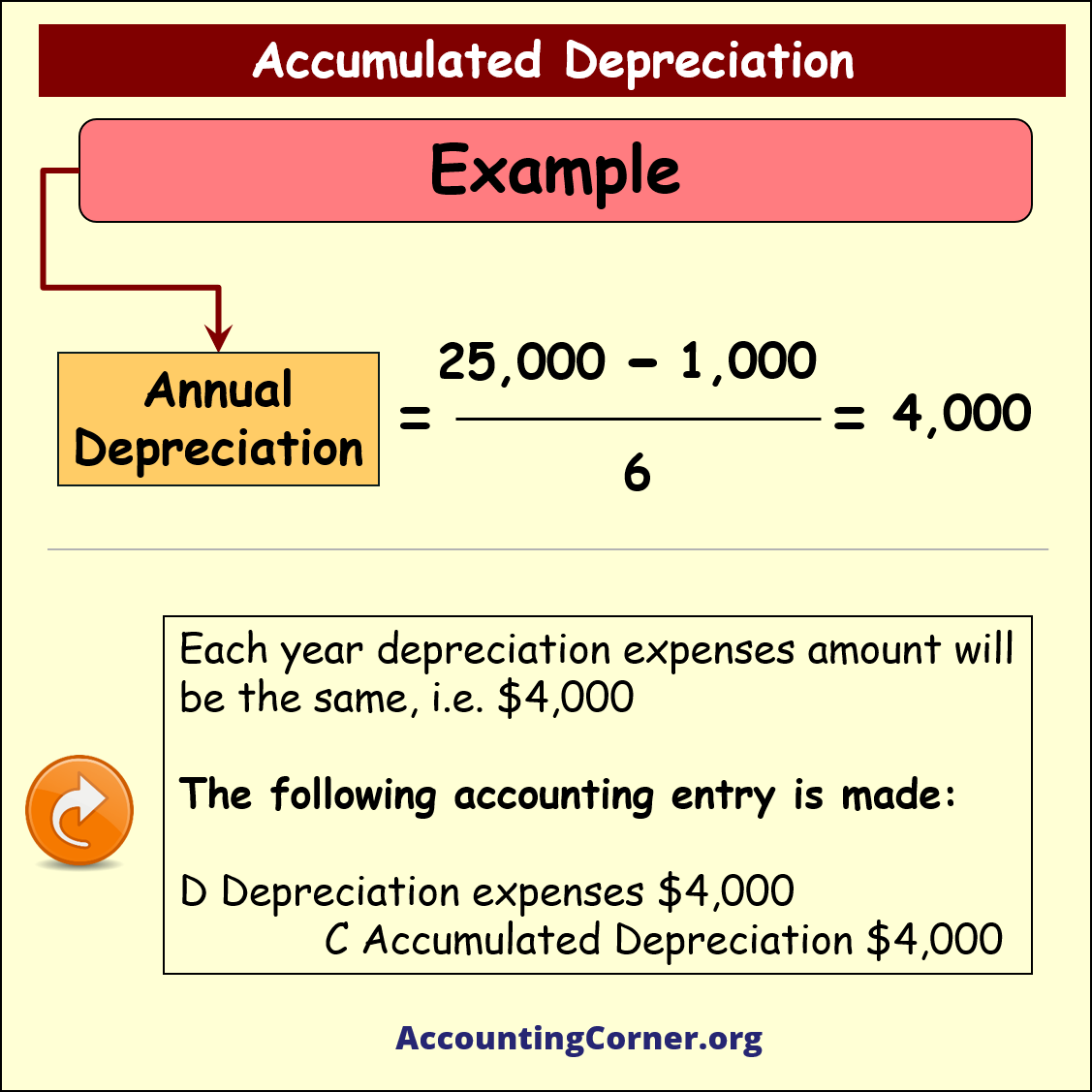

Annual Depreciation Calculation:

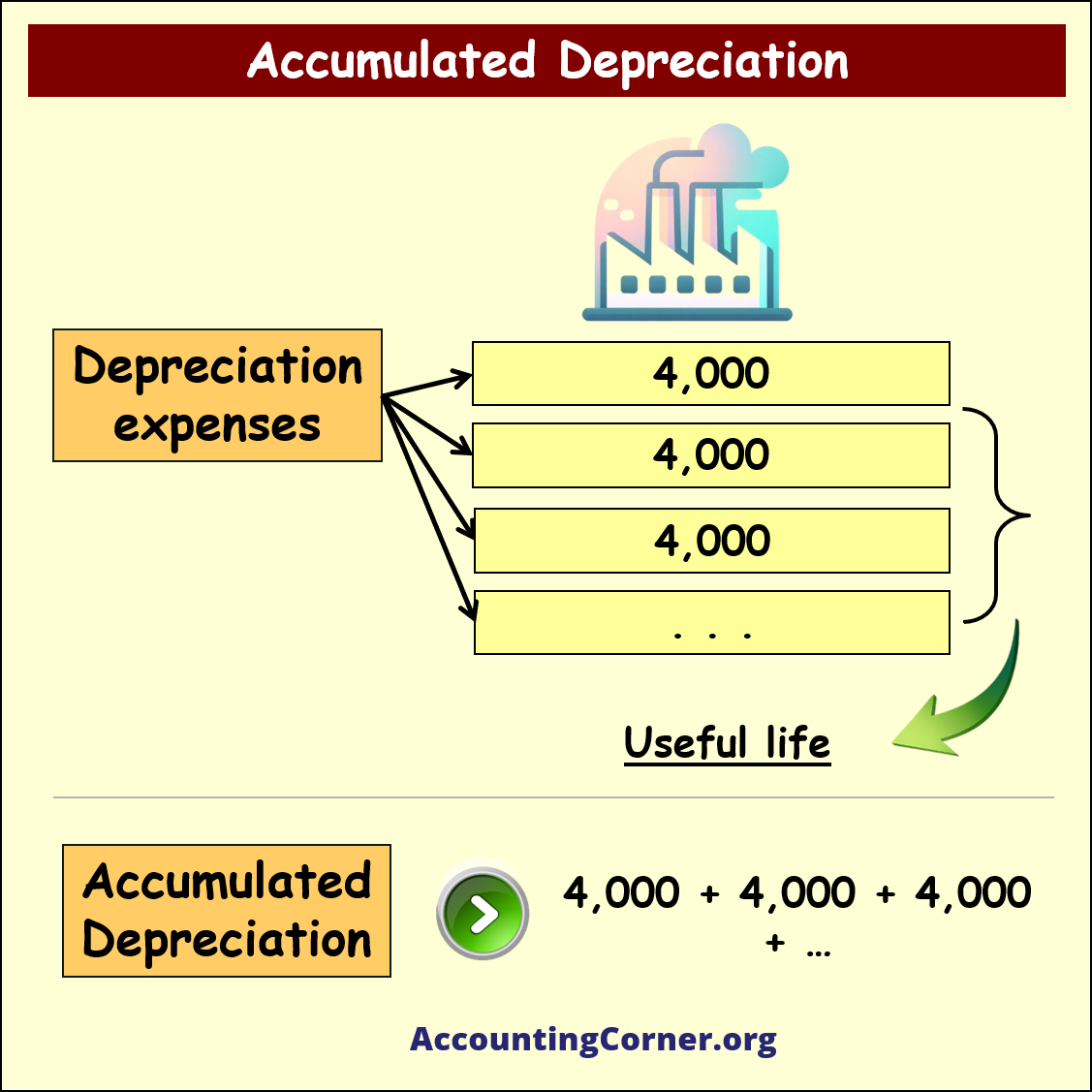

- Annual Depreciation = (Cost−Residual Value)/Useful Life = (25,000−1,000)/6 = 4,000

Each year, $4,000 will be recorded as depreciation expense, and this will accumulate over time.

Accounting Entries for Depreciation:

- Debit: Depreciation Expense $4,000

- Credit: Accumulated Depreciation $4,000

After three years, the total accumulated depreciation would be $12,000, and the net book value of the asset on the balance sheet would be:

- Net Book Value = Cost−Accumulated Depreciation = 25,000−12,000=13,000

Importance of Accumulated Depreciation

Accumulated depreciation plays a crucial role in financial reporting and asset management:

- Reflects Asset Usage: It shows how much of the asset’s cost has been expensed, providing insights into the wear and tear or obsolescence of the asset.

- Accurate Financial Statements: Depreciation helps companies present a more accurate value of their assets on the balance sheet, which is essential for investors, creditors, and management.

- Tax Deductibility: Depreciation expenses can be tax-deductible, reducing the company’s taxable income over the asset’s useful life.

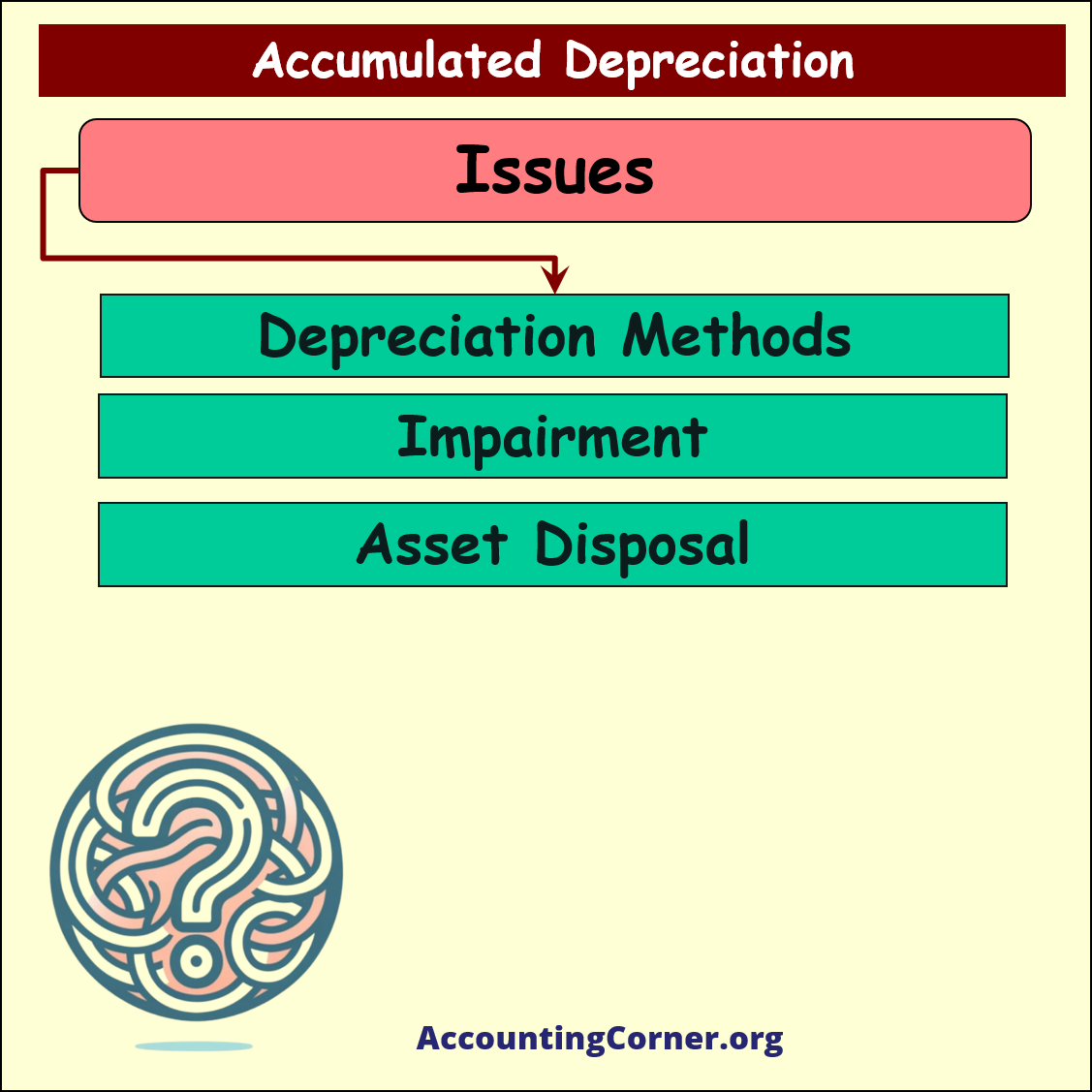

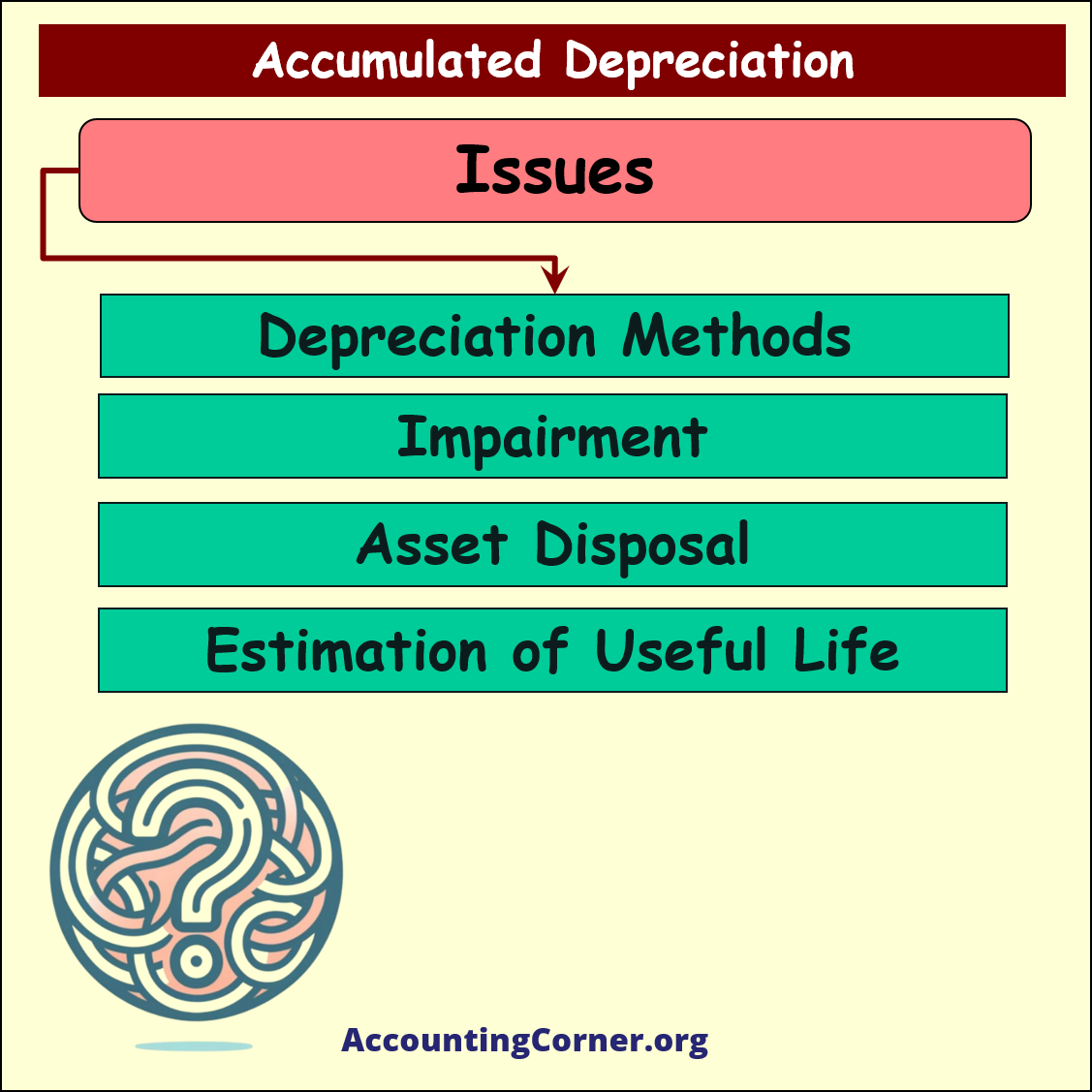

Issues and Considerations with Accumulated Depreciation

While accumulated depreciation is a straightforward accounting concept, there are several challenges and considerations:

- Depreciation Methods: Different depreciation methods, such as straight-line or declining balance, can result in varying amounts of accumulated depreciation over time.

- Impairment: If an asset becomes impaired or significantly loses value before the end of its useful life, additional adjustments may be needed to reflect the change in value.

- Asset Disposal: When a fixed asset is sold or retired, its accumulated depreciation needs to be removed from the balance sheet along with the asset’s cost.

- Estimating Useful Life: Accurately estimating the useful life of an asset can be challenging. A wrong estimate may lead to incorrect depreciation charges and accumulated depreciation balances.

Example of Accumulated Depreciation and Asset Disposal

When an asset is sold or retired, its cost and accumulated depreciation are removed from the balance sheet. Suppose a company sells the asset mentioned earlier after three years of use:

- Asset Cost: $25,000

- Accumulated Depreciation: $12,000 (after three years)

The net book value of the asset would be $13,000. If the company sells the asset for $15,000, the accounting entries would be:

- Debit: Cash $15,000

- Debit: Accumulated Depreciation $12,000

- Credit: Asset (Fixed Asset) $25,000

- Credit: Gain on Sale of Asset $2,000

Conclusion: Understanding Accumulated Depreciation

Accumulated depreciation is a key component of financial reporting, helping businesses allocate the cost of an asset over its useful life and providing a clear view of the asset’s value. It ensures that financial statements accurately reflect the asset’s usage and value, aiding in financial analysis and decision-making. Companies must carefully manage accumulated depreciation to avoid over- or under-valuing their assets.

Summary Points:

- 🏗 Definition: Total depreciation recorded against a fixed asset over its useful life.

- 💰 Depreciation Calculation: Formula based on the asset’s cost, residual value, and useful life.

- 🏦 Balance Sheet Impact: Accumulated depreciation reduces the book value of assets.

- ⚖️ Depreciation Methods: Straight-line, declining balance, and other methods impact how depreciation accumulates.

- 📉 Key Considerations: Impairment, asset disposal, and accurate estimates of useful life are crucial for proper accounting.

Accumulated depreciation provides critical insights into how a company uses its assets and the financial implications of those assets over time, ensuring transparent and accurate financial reporting.

Accumulated Depreciation – Visuals

Accumulated Depreciation – Video

The Most Popular Accounting & Finance Topics:

- Balance Sheet

- Balance Sheet Example

- Classified Balance Sheet

- Balance Sheet Template

- Income Statement

- Income Statement Example

- Multi Step Income Statement

- Income Statement Format

- Common Size Income Statement

- Income Statement Template

- Cash Flow Statement

- Cash Flow Statement Example

- Cash Flow Statement Template

- Discounted Cash Flow

- Free Cash Flow

- Accounting Equation

- Accounting Cycle

- Accounting Principles

- Retained Earnings Statement

- Retained Earnings

- Retained Earnings Formula

- Financial Analysis

- Current Ratio Formula

- Acid Test Ratio Formula

- Cash Ratio Formula

- Debt to Income Ratio

- Debt to Equity Ratio

- Debt Ratio

- Asset Turnover Ratio

- Inventory Turnover Ratio

- Mortgage Calculator

- Mortgage Rates

- Reverse Mortgage

- Mortgage Amortization Calculator

- Gross Revenue

- Semi Monthly Meaning

- Financial Statements

- Petty Cash

- General Ledger

- Allocation Definition

- Accounts Receivable

- Impairment

- Going Concern

- Trial Balance

- Accounts Payable

- Pro Forma Meaning

- FIFO

- LIFO

- Cost of Goods Sold

- How to void a check?

- Voided Check

- Depreciation

- Face Value

- Contribution Margin Ratio

- YTD Meaning

- Accrual Accounting

- What is Gross Income?

- Net Income

- What is accounting?

- Quick Ratio

- What is an invoice?

- Prudent Definition

- Prudence Definition

- Double Entry Accounting

- Gross Profit

- Gross Profit Formula

- What is an asset?

- Gross Margin Formula

- Gross Margin

- Disbursement

- Reconciliation Definition

- Deferred Revenue

- Leverage Ratio

- Collateral Definition

- Work in Progress

- EBIT Meaning

- FOB Meaning

- Return on Assets – ROA Formula

- Marginal Cost Formula

- Marginal Revenue Formula

- Proceeds

- In Transit Meaning

- Inherent Definition

- FOB Shipping Point

- WACC Formula

- What is a Guarantor?

- Tangible Meaning

- Profit and Loss Statement Template

- Revenue Vs Profit

- FTE Meaning

- Cash Book

- Accrued Income

- Bearer Bonds

- Credit Note Meaning

- EBITA meaning

- Fictitious Assets

- Preference Shares

- Wear and Tear Meaning

- Cancelled Cheque

- Cost Sheet Format

- Provision Definition

- EBITDA Meaning

- Covenant Definition

- FICA Meaning

- Ledger Definition

- Allowance for Doubtful Accounts

- T Account / T Accounts

- Contra Account

- NOPAT Formula

- Monetary Value

- Salvage Value

- Times Interest Earned Ratio

- Intermediate Accounting

- Mortgage Rate Chart

- Opportunity Cost

- Total Asset Turnover

- Sunk Cost

- Housing Interest Rates Chart

- Additional Paid In Capital

- Obsolescence

- What is Revenue?

- What Does Per Diem Mean?

- Unearned Revenue

- Accrued Expenses

- Earnings Per Share

- Consignee

- Accumulated Depreciation

- Leashold Improvements

- Operating Margin

- Notes Payable

- Current Assets

- Liabilities

- Controller Job Description

- Define Leverage

- Journal Entry

- Productivity Definition

- Capital Expenditures

- Check Register

- What is Liquidity?

- Variable Cost

- Variable Expenses

- Cash Receipts

- Gross Profit Ratio

- Net Sales

- Return on Sales

- Fixed Expenses

- Straight Line Depreciation

- Working Capital Ratio

- Fixed Cost

- Contingent Liabilities

- Marketable Securities

- Remittance Advice

- Extrapolation Definition

- Gross Sales

- Days Sales Oustanding

- Residual Value

- Accrued Interest

- Fixed Charge Coverage Ratio

- Prime Cost

- Perpetual Inventory System

- Vouching

Return from Accumulated Depreciation to AccountingCorner.org home